India's B2B trade finance market is valued at $800B+ annually, supporting the country's huge export-import economy. Yet access to finance remains difficult—SMEs struggle with collateral requirements, lengthy approval processes (30-90 days), and opaque lending criteria. Banks dominate, but technology adoption is minimal.

Key Opportunity: Build an AI-first trade finance platform that assesses creditworthiness through alternative data, evaluates collateral smarter, and enables near-instant approvals.1.

Executive Summary

2.

Problem Statement

Who Experiences This Pain?

- Exporters needing working capital for order fulfillment

- Importers requiring letter of credit facilities

- Manufacturer SMEs lacking fixed collateral

- Trading companies with strong orders but weak balance sheets

- Freight forwarders needing equipment financing

- Agricultural exporters facing seasonal cash flows

The Pain Points

| Pain Point | Impact | Current "Solution" |

|---|---|---|

| Collateral requirements | 70% of loan rejections | Real estate or gold pledge |

| Lengthy approval | 30-90 day processing | Lose orders to competitors |

| Opaque criteria | Don't know why rejected | Multiple bank applications |

| Documentation overhead | 50+ documents per application | CAcertified statements |

| Currency risk | Exchange rate losses | Manual hedging |

| Cross-border complexity | LC processing delays | Established relationships |

3.

Current Solutions

| Company | What They Do | Why They're Not Solving It |

|---|---|---|

| SBI Trade Finance | Government bank trade finance | Slow, paper-heavy, branch-dependent |

| ICICI Bank Trade | Corporate trade finance | Enterprise focus, not SME-friendly |

| Axis Bank Trade | Trade finance services | Documentation heavy |

| Creditas | Supply chain finance | Early stage, limited coverage |

| Proto | Trade finance | Focused on a few verticals |

| WhatsApp Lenders | Informal financing | High interest, Unregulated |

Why Incumbents Will Struggle

Indian banks view trade finance as low-margin, high-risk. Technology investment is minimal—core banking systems from the 1990s still dominate. A new entrant focused purely on trade finance with AI can dramatically improve turnaround times and accept risk profiles traditional banks reject.

4.

Market Opportunity

Market Size

- India B2B trade finance: $800B+ (2026)

- Export credit: $200B+

- Import financing: $300B+

- Supply chain finance: $150B+

- Addressable (AI-capable): $250B+

Growth Drivers

Why Now

- UPI success: Digital payment infrastructure proven

- Account aggregation: AA ecosystem maturing

- Data availability: GST, income tax data digital

- WhatsApp penetration: Native distribution channel

- No AI-first entrant: Greenfield opportunity

5.

Gaps in the Market

Gap 1: Alternative Credit Assessment

No platform analyzes alternative data (GST returns, invoice history, shipping signals, utility payments) to assess creditworthiness beyond traditional metrics.Gap 2: Smart Collateral Evaluation

No platform properly values movable assets, purchase orders, or inventory as collateral—focus is on real estate.Gap 3: Cross-Border Trade Finance

No unified platform handles import LC, export advance, and forex requirements with integrated processing.Gap 4: Supply Chain Finance

No platform connects buyers, suppliers, and financiers for dynamic discounting and reverse factoring.Gap 5: Instant Approvals

Traditional banks take weeks. No platform offers hours-level approvals for pre-qualified businesses.6.

AI Disruption Angle

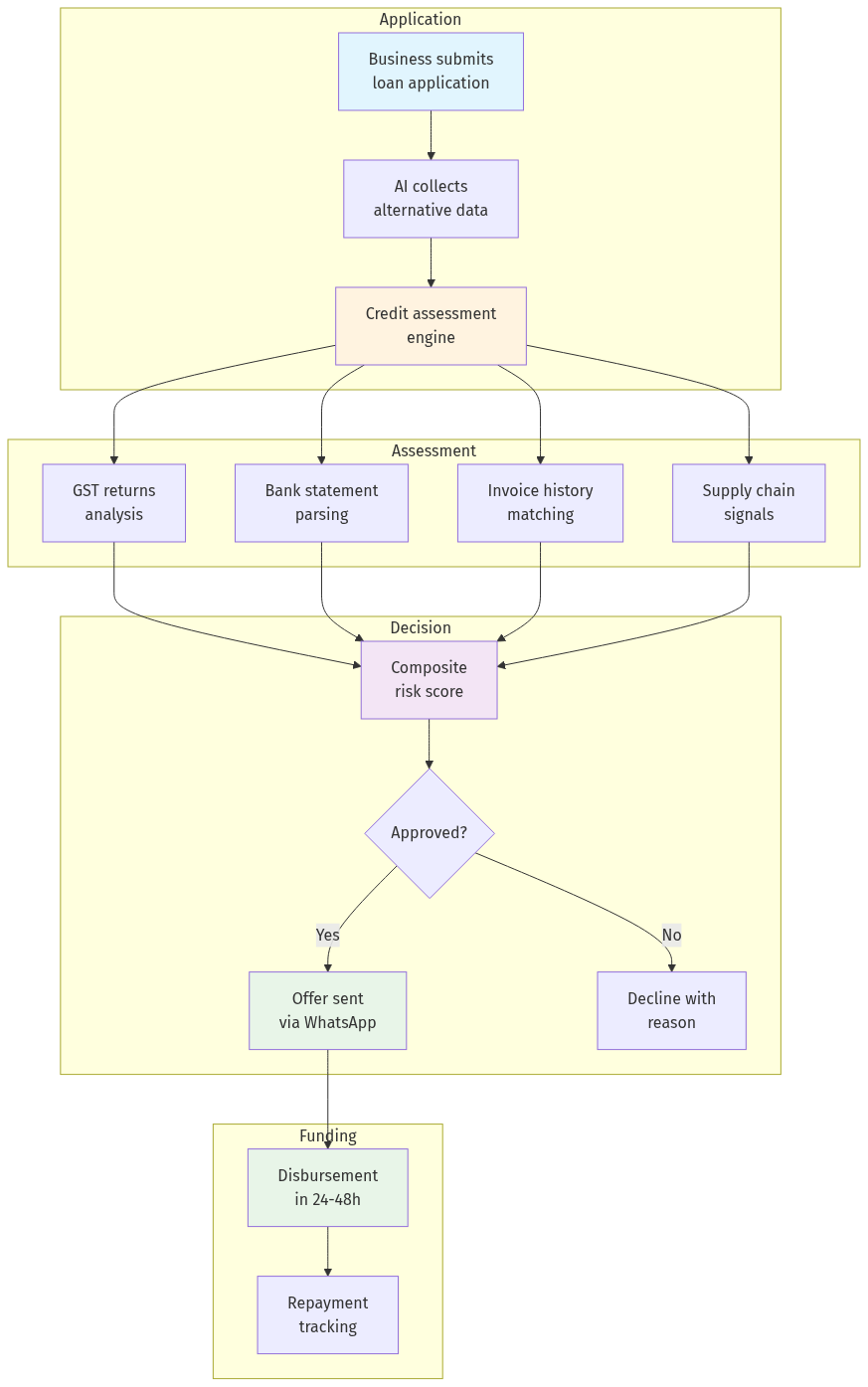

Today's Workflow

Exporter → Visit bank branch → Submit 50+ documents → Wait 30-90 days → Collateral evaluation → Maybe approved → Funds releasedWith AI Platform

Exporter → WhatsApp/Upload application → AI analyzes alt data (hours) → Smart collateral valuation → Offer sent via WhatsApp → 24-48h disbursement

Key AI Capabilities

7.

Product Concept

Core Features

| Feature | Description |

|---|---|

| Alt Credit Score | AI-generated score from 20+ data points |

| Fast Approval | 24-48h approval for qualified applicants |

| Smart Collateral | Moveable asset acceptance |

| Invoice Financing | Post-delivery financing |

| LC Processing | Import/export letter of credit |

| Currency Hedging | Embedded forex options |

| WhatsApp Channel | Full application via WhatsApp |

User Flows

Buyer Flow:8.

Development Plan

| Phase | Timeline | Deliverables |

|---|---|---|

| MVP | 8 weeks | Alt credit scoring, WhatsApp flow, 10 lenders |

| V1 | 12 weeks | Collateral evaluation, invoice financing |

| V2 | 16 weeks | LC processing, currency hedging |

| V3 | 20 weeks | Multi-country expansion, trade repo |

Tech Stack

- Backend: Node.js/PostgreSQL

- AI: Python for credit modeling, LangChain for NLP

- WhatsApp: Kapso API

- Banking: Account Aggregator (AA) API

- Payments: Razorpay/Yes Bank

9.

Go-To-Market Strategy

Phase 1: Export Hotspots (Months 1-3)

Phase 2:Importer Expansion (Months 3-6)

Phase 3: Scale (Months 6-12)

10.

Revenue Model

| Stream | Description | Margin |

|---|---|---|

| Processing Fee | 0.5-1% on funded amounts | 0.5-1% |

| Interest Spread | 3-5% between funder and borrower | 3-5% |

| Gateway Fee | Payment facilitation | 0.1-0.2% |

| Currency Services | Forex hedging margins | 0.5-1% |

| Data Services | Market intelligence reports | ₹50000-200000/report |

11.

Data Moat Potential

Proprietary Data That Accumulates

Why This Creates Moat

- New entrants need to build scoring history

- Borrower relationships are sticky

- Lender trust takes time to establish

- Data network effects compound

12.

Why This Fits AIM Ecosystem

Vertical Synergies

| Existing Asset | Integration Point |

|---|---|

| Industrial supplies | Financing for purchases |

| Packaging materials | Working capital |

| Construction materials | Contractor finance |

| Domain portfolio | tradefinance.in, b2bfinance.in |

Shared Infrastructure

- WhatsApp workflow (already built)

- Trust scoring (adapted)

- Payment infra (shared)

- Supplier network (leverageable)

## Verdict

Opportunity Score: 9/10

| Factor | Score | Rationale |

|---|---|---|

| Market size | 10/10 | $800B+, growing |

| Timing | 9/10 | Data infra ready |

| Competition | 8/10 | Fragmented banks only |

| Moat potential | 9/10 | Alt data compound |

| GTM complexity | 7/10 | Cluster-based approach needed |

Recommendation

BUILD. Trade finance is massive, fragmented, and ripe for AI transformation. WhatsApp-native + alt credit data + fast approvals differentiate. Key: Build lender network first, then borrower demand.Watch Outs

- Regulatory compliance (RBI/SEBI)

- Currency risk management

- Fraud prevention critical

- Lender concentration risk

## Appendix: Traditional vs AI Workflow

┌─────────────────────────────────────────────────────────────┐

│ TRADITIONAL BANK WORKFLOW │

├─────────────────────────────────────────────────────────────┤

│ 1. Visit bank branch (physically) │

│ 2. Fill lengthy application form │

│ 3. Submit 50+ documents (photocopies) │

│ 4. Wait 30-90 days for processing │

│ 5. Collateral evaluation (real estate) │

│ 6. Committee approval (weekly meet) │

│ 7. Possibly approved or rejected │

│ 8. Additional documentation requests │

│ 9. Loan disbursal │

└─────────────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────────┐

│ AI PLATFORM WORKFLOW │

├─────────────────────────────────────────────────────────────┤

│ 1. Apply via WhatsApp (text/voice) │

│ 2. Auto-connect GST, bank statements (with permission) │

│ 3. AI analyzes 20+ alternative data points (minutes) │

│ 4. Smart collateral valuation │

│ 5. Composite risk score generated │

│ 6. Approved/reject with reason │

│ 7. Offer sent via WhatsApp with term sheet │

│ 8. Digital agreement execution │

│ 9. Funds disbursed in 24-48 hours │

└─────────────────────────────────────────────────────────────┘❧