India has a credit paradox: Banks have ₹80L Cr of lending capital but won't lend to MSMEs because they can't assess risk. Meanwhile, 63 million MSMEs are actively serving customers, generating revenue, paying taxes — but have no "credit history" in the traditional sense.

The solution isn't better banks. It's alternative data credit scoring — using non-traditional signals to build financial identities where none exist.

Key Opportunity:- India has 48 million "credit-invisible" MSMEs with zero CIBIL/CRT score

- 73% of SME loan applications are rejected due to "insufficient credit history"

- Average 187 days to secure a ₹10L working capital loan

- Digital lending has grown 340% but mostly to already-bankable segment

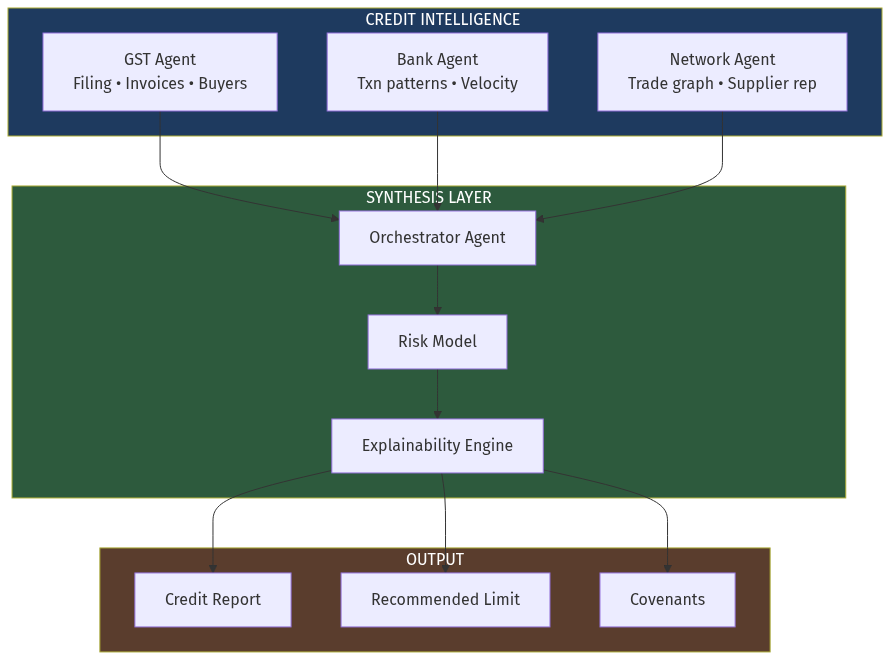

- GST return patterns (growth trend, consistency, tax compliance)

- Bank statement transactions (cash flow, payroll, supplier payments)

- Utility/bill payment history (operational continuity)

- Supply chain data (orders, fulfillment, customer concentration)

- UPI/POS transaction history (daily revenue patterns)