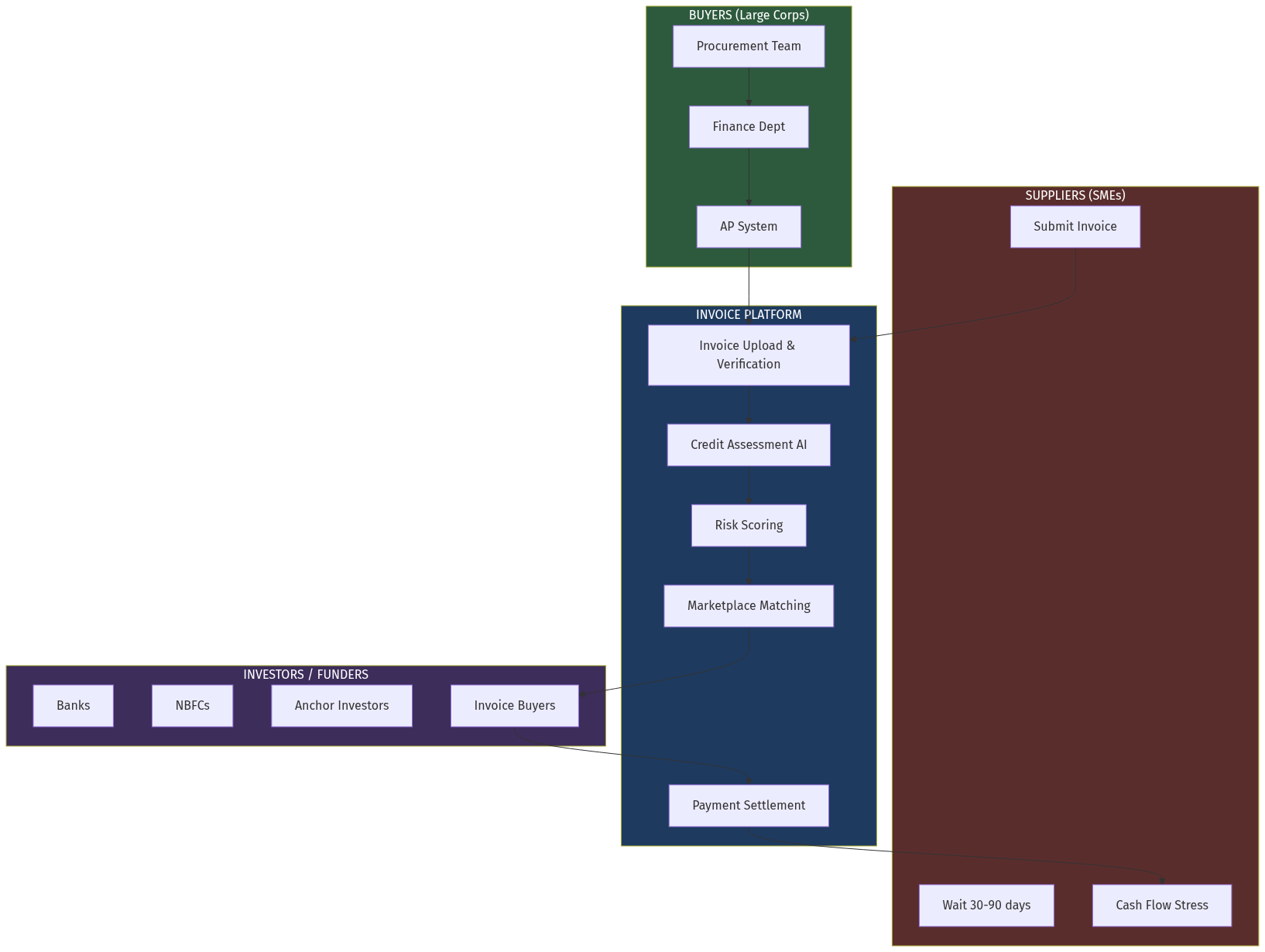

India's SME sector contributes 30% of GDP and employs 110 million people. Yet these businesses face a chronic $300+ billion working capital gap due to delayed payments from large buyers. Invoice discounting—a $12 trillion global market—remains largely untapped in India due to manual processing, high transaction costs, and trust deficits between buyers, sellers, and funders.

AI agents can automate credit assessment, verify invoice authenticity in real-time, and create a liquid marketplace for invoice trading. This article explores the opportunity to build India's first AI-native invoice discounting platform.