India's MSME sector contributes 30% of GDP and employs 110 million people. Yet these businesses receive less than 20% of bank credit despite being the nation's economic backbone. The root cause isn't demand — it's verification.

Banks and NBFCs require collateral verification before lending, but the process is broken: property documents are physical, machinery records are scattered across factories, inventory is invisible, and receivables are untracked. Manual verification costs ₹15,000-50,000 per loan and takes 3-8 weeks.

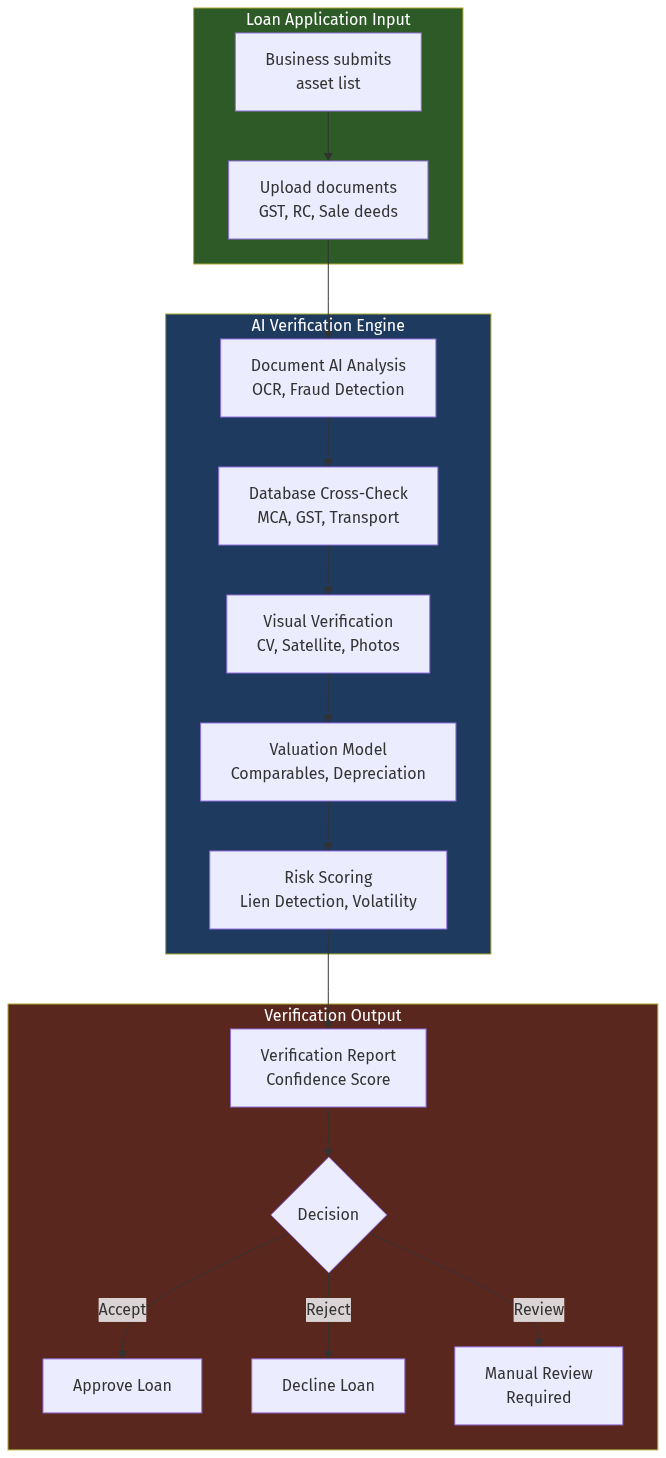

This article explores how AI-powered asset verification agents can transform MSME lending — by digitizing collateral assessment, automating verification workflows, and building the first comprehensive asset registry for Indian businesses. The opportunity: enable $500B in new MSME credit over the next decade.