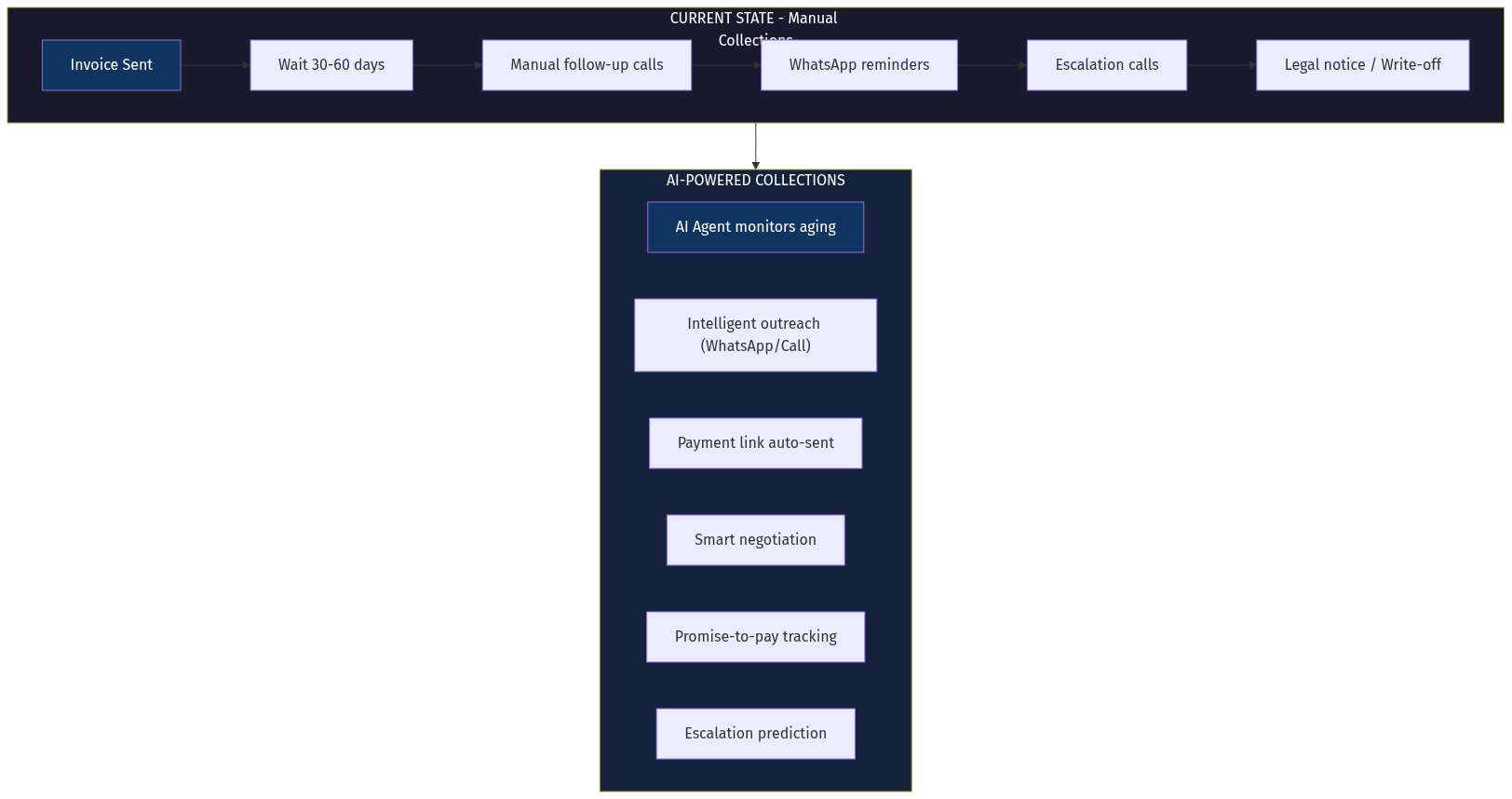

India's B2B economy runs on credit. Manufacturers supply to distributors, distributors sell to retailers, and everyone pays 30-90 days later. But the infrastructure for managing this credit lifecycle remains shockingly primitive.

While fintech has solved lending and payments, the operational work of collecting payments — the calls, the WhatsApp messages, the follow-ups, the negotiations — remains almost entirely manual. This creates a massive opportunity for AI-powered collections agents.

This article explores the gap in B2B collections automation in India, why it persists, and how AI agents can transform a $23 billion market.