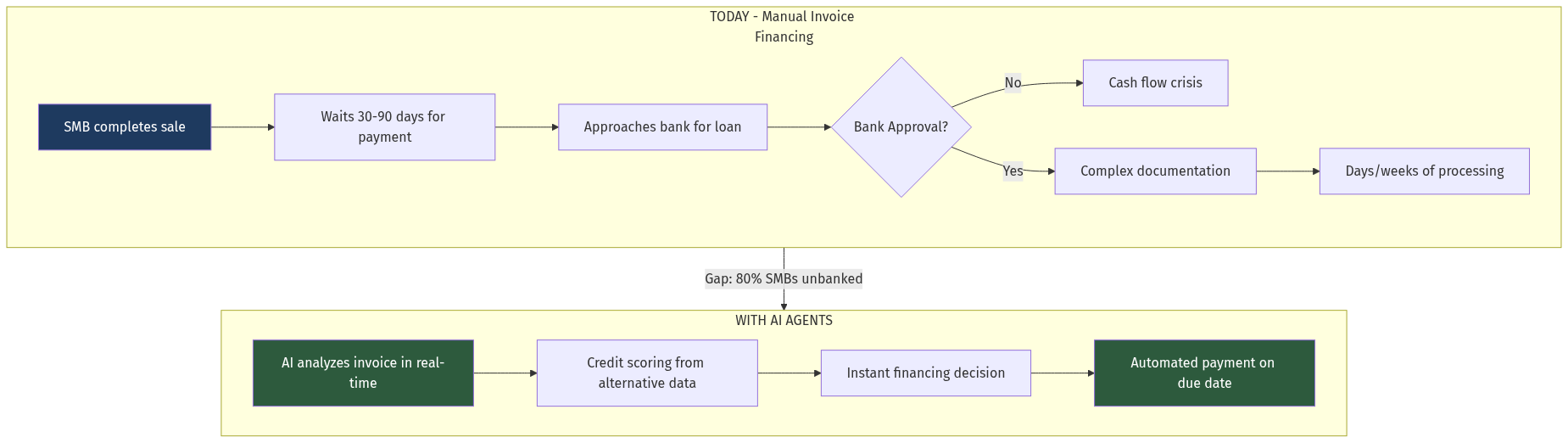

B2B invoice financing (also called receivable discounting or invoice factoring) represents one of the largest untapped opportunities in Indian fintech. With $120 billion in outstanding SME receivables and a 47-day average payment cycle, Indian SMBs are bleeding cash while waiting for payments. Traditional banks, with their 12-15% interest rates and 3-week processing times, serve less than 20% of this market.

AI-powered invoice financing platforms can reduce approval times from weeks to seconds, serve the 80% of SMBs that banks reject, and build proprietary credit datasets that become defensible moats over time.