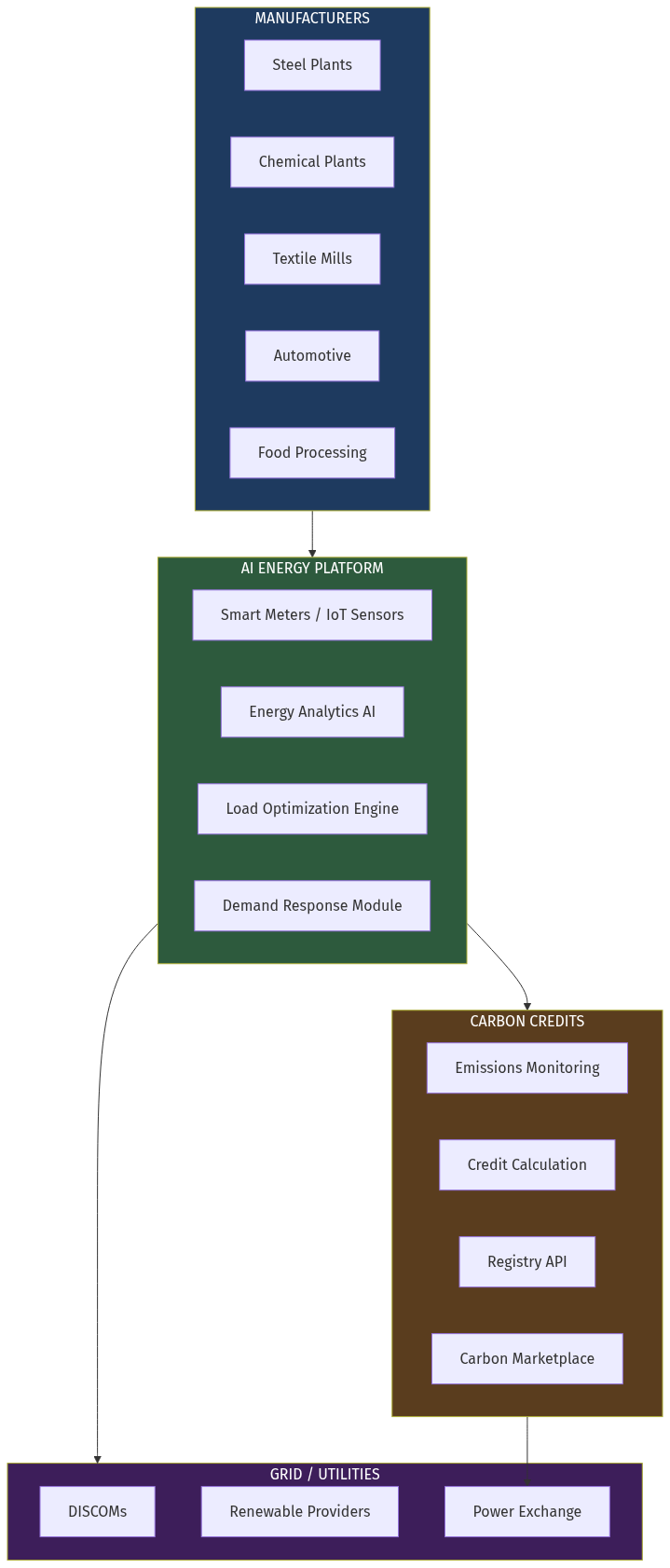

India's industrial energy sector stands at an inflection point. With DISCOM losses exceeding ₹90,000 crore annually, renewable penetration targets of 50% by 2030, and emerging carbon credit markets, there's unprecedented opportunity for AI-powered energy management platforms that simultaneously reduce costs and generate new revenue streams through carbon credits.

This article proposes an AI-powered industrial energy management and carbon credits marketplace — a platform that combines real-time energy monitoring, predictive optimization, demand response orchestration, and carbon credit generation into a unified offering for manufacturing plants across India.

Opportunity Score: 8.5/10