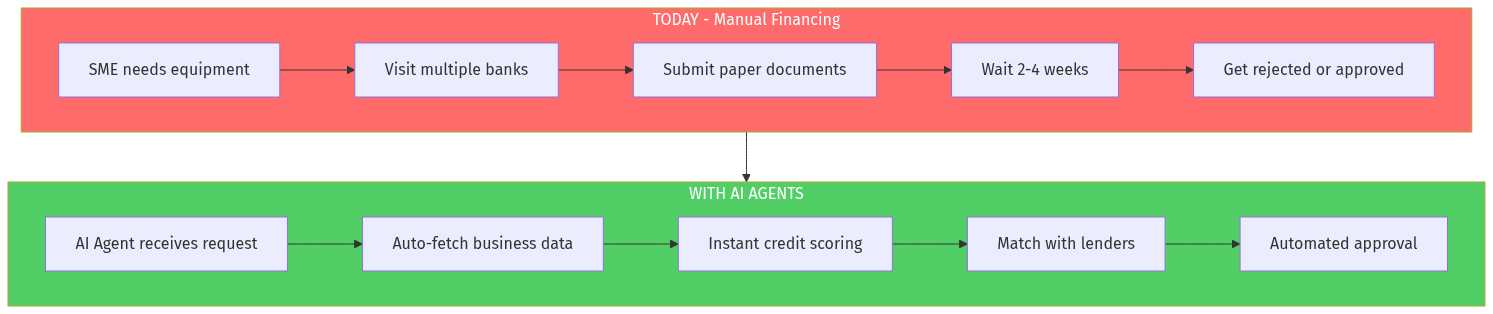

India's 63 million micro, small, and medium enterprises (MSMEs) face a $50+ billion financing gap. Equipment financing—a critical enabler for business growth—remains stuck in manual, paper-heavy processes with 40%+ rejection rates and 2-4 week turnaround times.

This article proposes an AI-powered B2B equipment financing marketplace that automates the entire lending workflow: from instant credit scoring using alternative data, to matching SMEs with the right lenders, to automated document processing and near-instant approval.

Opportunity Score: 8.5/10