The Indian infrastructure materials market for RCC pipes, precast concrete products, and drainage systems is a $12 billion industry that operates almost entirely offline. Despite the digital transformation of adjacent markets (steel via OfBusiness, general B2B via IndiaMART), specialized infrastructure materials remain trapped in fragmented supply chains characterized by price opacity, logistical complexity, and limited supplier discovery.

Our research identified 207+ RCC pipe manufacturers across 21 Indian states, with heavy concentration in Haryana (21), Gujarat (20), and Maharashtra (18). Yet contractors still source these materials through local dealers with limited options, manual price negotiations, and no quality standardization.

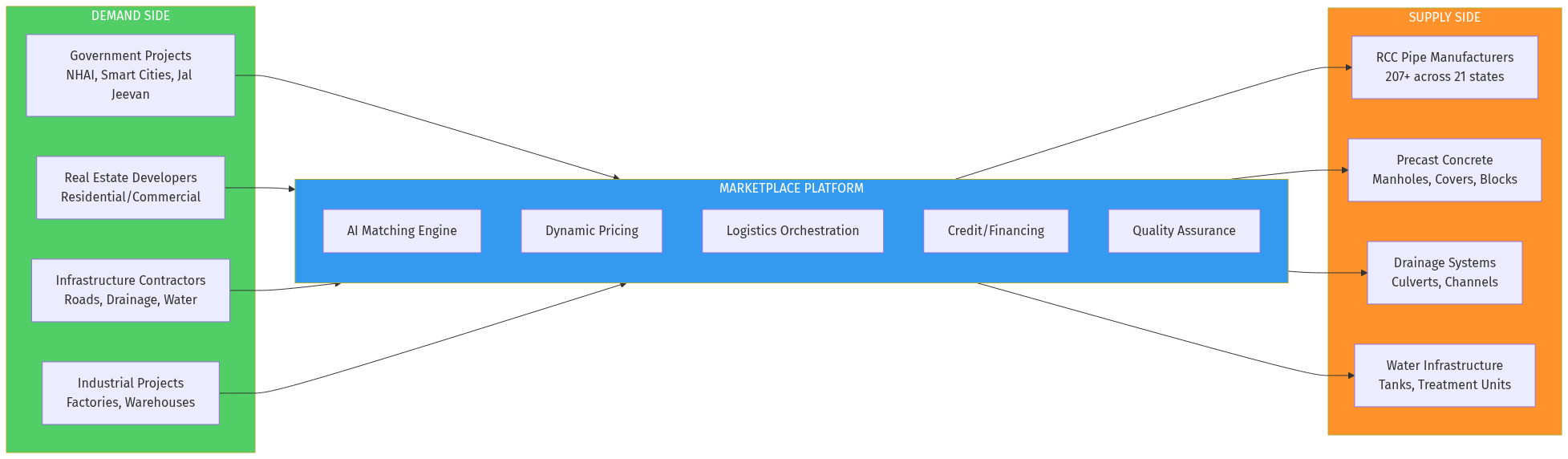

The opportunity: Build a vertical B2B marketplace that connects infrastructure contractors directly with manufacturers, powered by AI-driven matching, dynamic pricing, and integrated logistics—similar to what OfBusiness built for steel and cement, but specialized for bulky, logistics-heavy infrastructure materials.