Direct Alignment

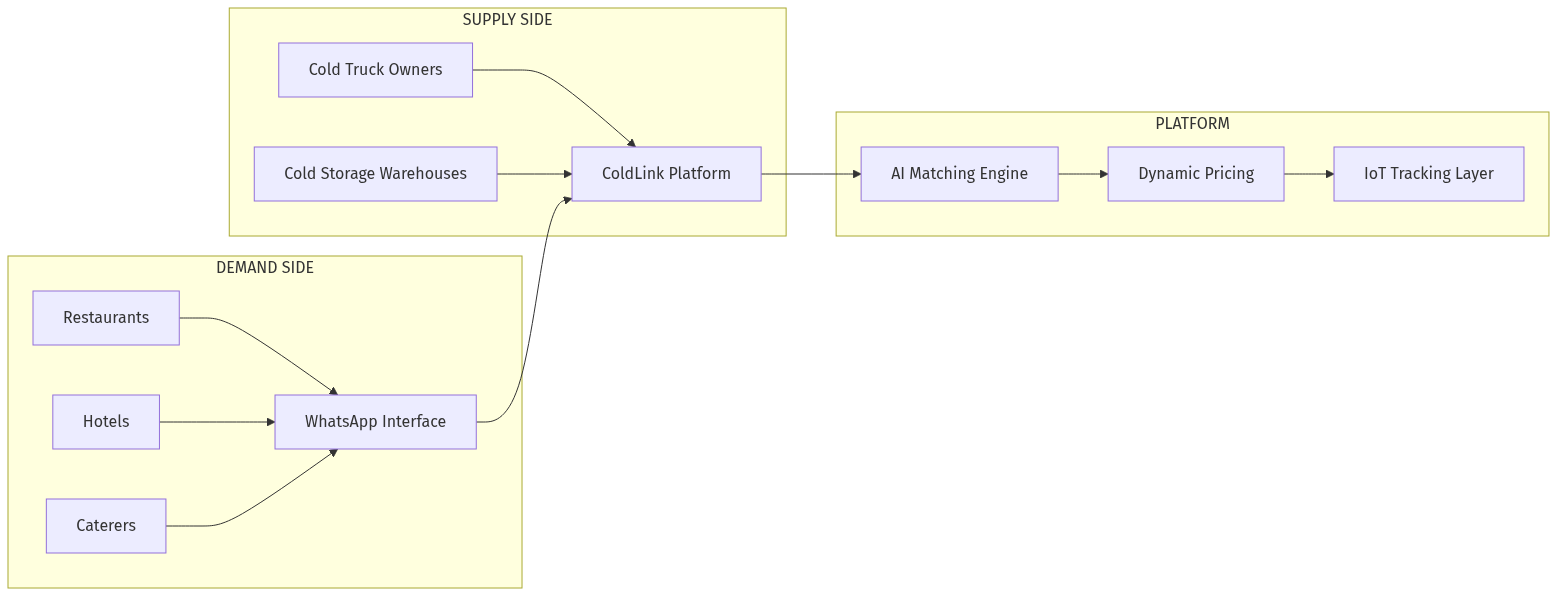

B2B Marketplace: Connects fragmented supply (reefer fleets) with demand (shippers)

Workflow Automation: Replaces phone/WhatsApp booking with intelligent matching

AI-Native: Core value from AI (matching, prediction, compliance automation)

India-First: Solving uniquely Indian cold chain fragmentation

Repeat Transactions: Daily/weekly shipments create recurring platform usage

Cross-Vertical Synergies

- Pharma vertical: Links to medical equipment, diagnostic lab logistics

- Food vertical: Connects to restaurant procurement, FSSAI compliance

- Agriculture vertical: Farm-to-fork cold chain for produce aggregators

AIM Data Network

- Cold chain intelligence becomes a horizontal capability

- Cross-pollination with other logistics verticals

- Unified B2B transaction layer

## Mental Models Applied

Zeroth Principles

Assumption questioned: "Cold chain is a hardware/infrastructure problem"

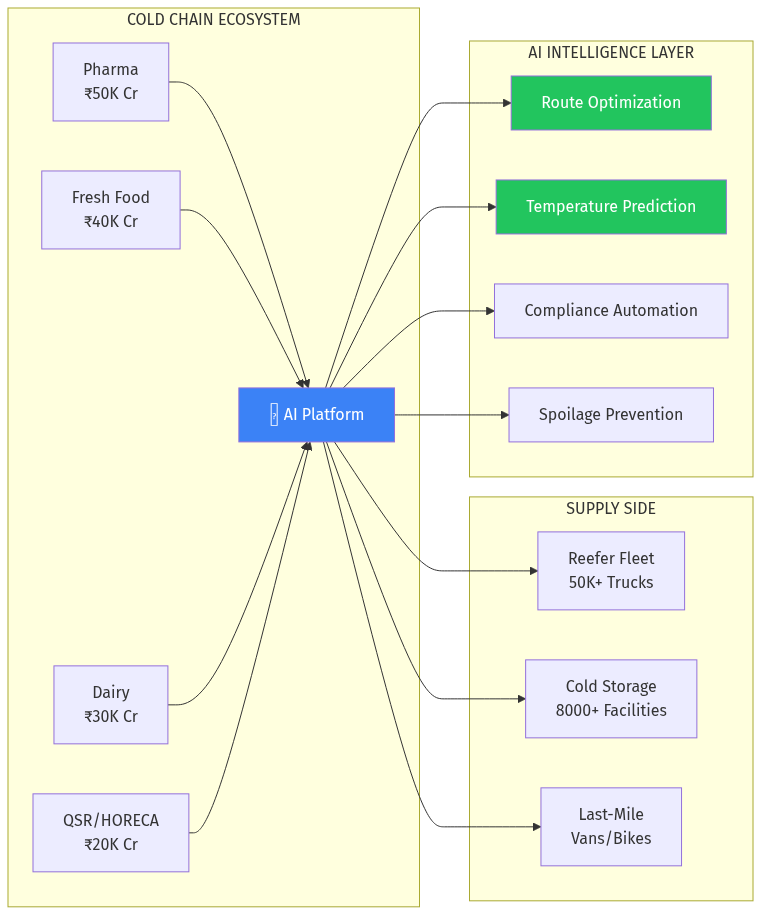

Reframe: Cold chain is an information problem. The infrastructure exists (50K reefer trucks, 8K cold storages). The failure is coordination, visibility, and intelligence.

Incentive Mapping

- Fleet operators want utilization — currently 50-60%, could be 80%+

- Shippers want compliance proof — currently manual and expensive

- Regulators want visibility — currently impossible to audit

- All incentives align toward a digital platform

Distant Domain Import

Imported from: Energy grid management

- Grid operators balance supply/demand in real-time across distributed assets

- Cold chain is similar: distributed temperature-controlled assets needing orchestration

- Predictive load balancing → Predictive spoilage prevention

Falsification (Pre-Mortem)

Why might this fail?

Fleet operators resist IoT installation → Offer hardware subsidies, show utilization gains

Shippers already have 3PL relationships → Position as intelligence layer, not competitor

Data accuracy issues with cheap sensors → Partner with validated IoT providers

Regional players dominate local routes → Start with high-compliance pharma where national platform needed

Steelmanning (Why Incumbents Might Win)

- Snowman/Kool-ex have existing relationships and owned assets

- Counter: They can't aggregate fragmented capacity; platform model scales faster

- Large 3PLs (DHL, Maersk) entering India cold chain

- Counter: Global players struggle with India's fragmentation; local platform has advantage

Anomaly Hunting

Strange observation: India has 50K+ reefer trucks but 40% food wastage

Explanation: Trucks exist but utilization is poor due to information asymmetry

Opportunity: Platform that increases utilization from 55% to 80% = massive value creation

## Verdict

Opportunity Score: 8.5/10

Strengths:

- Massive market (₹1.4L Cr) with clear pain points

- Regulatory tailwinds (FSSAI, pharma GDP)

- Fragmented supply perfect for marketplace aggregation

- AI adds genuine value (not just digitization)

- Strong data moat potential

Risks:

- Capital-intensive if hardware subsidy needed for IoT

- Cold chain has thin margins — need volume scale

- Incumbent relationships may be sticky

Recommendation:

Start with pharma corridor (highest compliance needs, premium pricing tolerance), prove the model, then expand to food/dairy. Partner with IoT hardware providers rather than building own sensors. Position as intelligence layer that complements existing 3PLs rather than competing directly.

This is a Tier 1 opportunity for the AIM ecosystem — high TAM, clear AI angle, strong India focus, and potential for cross-vertical expansion.

## Sources