AIM.in Alignment

- B2B marketplace DNA: Kiranas are India's largest B2B buyer network

- AI-first: Voice agents and demand prediction as core differentiators

- India-specific: This problem is uniquely Indian — no copy-paste from West

- WhatsApp-native: Builds on AIM's messaging-first philosophy

Integration Opportunities

- Supplier discovery: Kiranas find new distributors via AIM

- Category expansion: Same platform for electrical, hardware, pharma retail

- Cross-vertical data: Kirana demand signals inform manufacturer/supplier insights

Portfolio Synergy

- Domain:

kirana.in / dukaan.ai / munshi.ai available for acquisition

- Existing contacts: Distributor network from RCC pipes work

- Voice AI stack: Already built for other AIM verticals

## Mental Models Applied

Zeroth Principles

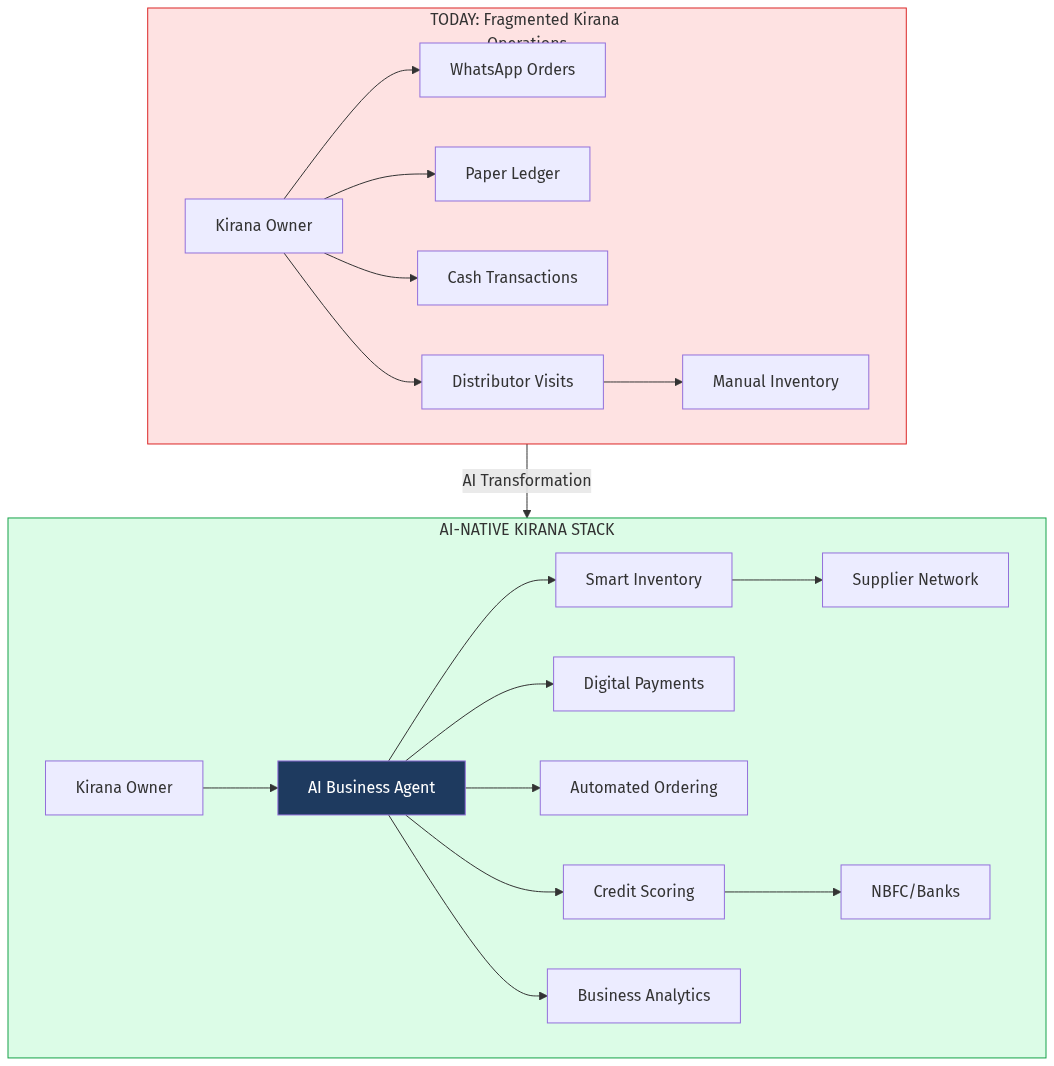

Assumption challenged: "Kiranas need apps to digitize."

Reality: They need a

person (even if AI) who speaks their language and manages their business. The interface is irrelevant — the relationship matters.

Incentive Mapping

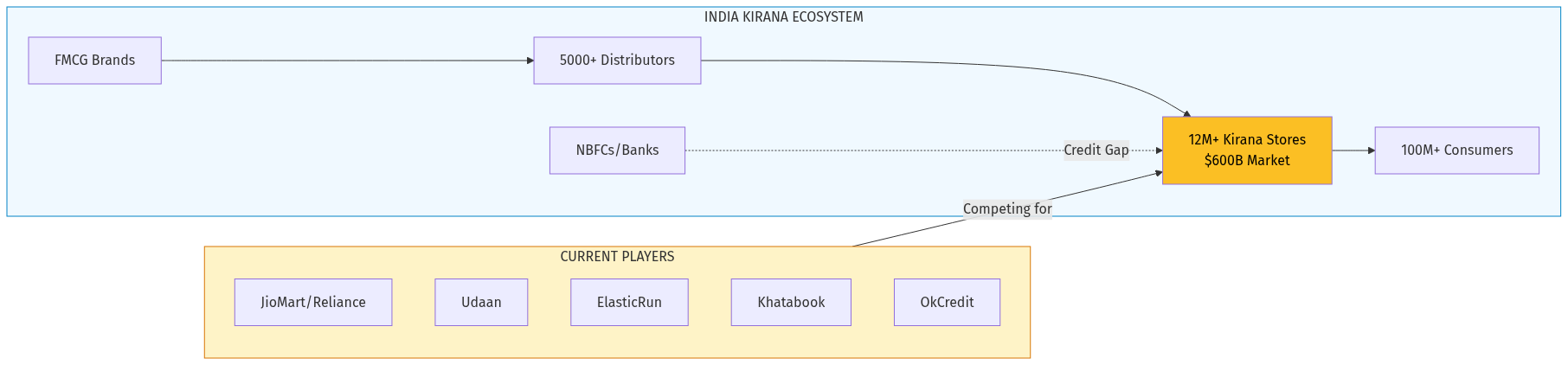

- Kirana owner: Wants more profit, less stress, credit access

- Distributor: Wants higher order frequency, lower collection effort

- Brand: Wants attribution and direct kirana relationship

- NBFC: Wants underwriting data and distribution

All incentives align toward a single intelligent layer that serves everyone.

Distant Domain Import

From: Restaurant POS systems (Toast, Square)

Import: The POS became the restaurant's OS, then added payments, payroll, lending.

Application: The kirana AI agent becomes the OS, then adds procurement, credit, analytics.

Falsification (Pre-Mortem)

Why might this fail?

Khatabook/OkCredit fatigue: Kiranas burned by overpromising apps → Solution: Distributor-led adoption, not direct sales

Voice AI not ready: Regional language accuracy insufficient → Solution: Hybrid (voice + simple button responses)

Low willingness to pay: Kiranas won't pay for software → Solution: Distributor/brand subsidized initially

Steelmanning Incumbents

Why JioMart might win:

- Reliance has distribution and capital

- Can offer credit at scale

- Already has 2M+ partner kiranas

Counter: Reliance wants kiranas to sell JioMart products. We want kiranas to sell whatever's best for them. The neutral platform wins long-term trust.

Anomaly Hunting

Strange fact: Khatabook reached 10M downloads but <500K active users.

Interpretation: Kiranas downloaded because of hype, churned because of low utility.

Opportunity: The bar for retention is low — consistent utility wins.

## Verdict

Opportunity Score: 9/10

Why this matters:

- Massive market ($600B) with proven digitization demand

- Clear gaps in existing solutions (voice, intelligence, credit linkage)

- AI cost economics finally viable for ₹300/month pricing

- Multiple revenue streams reduce dependency risk

- Data moat potential is enormous

Risks:

- Execution complexity (regional languages, last-mile onboarding)

- Incumbent retaliation (JioMart, Udaan)

- Regulatory uncertainty around NBFC partnerships

Recommendation: This is a

Tier-1 opportunity for AIM. Consider acquiring

munshi.ai or

dukaan.ai domain, building MVP in Q1, and targeting Tier-2 city distributor partnerships for validation.

The kirana store isn't dying — it's evolving. The question is who becomes its intelligent backbone.

## Sources