Strategic Alignment

B2B Marketplace DNA

- Aggregates fragmented demand (MSMEs) with fragmented supply (RE developers)

- Discovery + transaction + fulfillment in one platform

- High-value, repeat transactions

India-Specific Opportunity

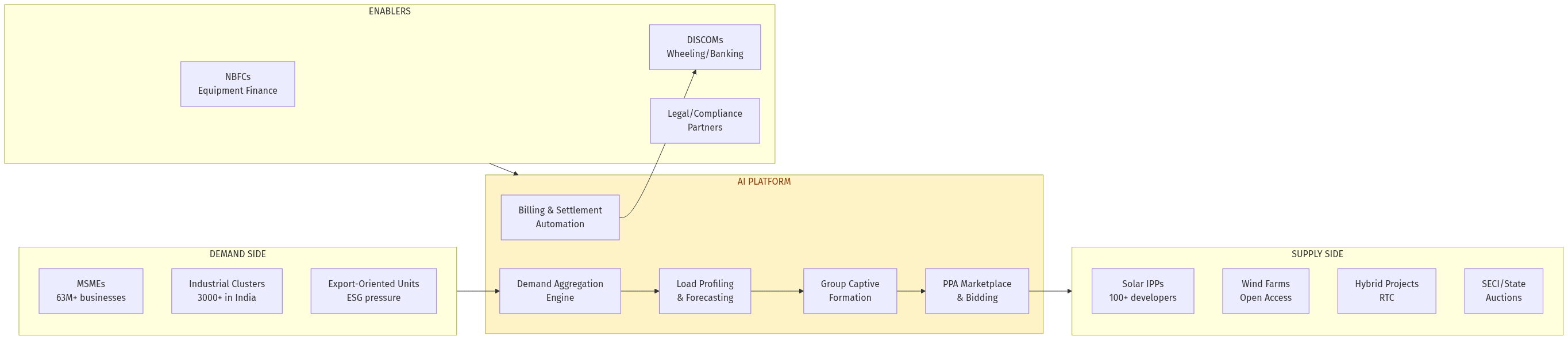

- 63M MSMEs, 3000+ industrial clusters

- Regulatory complexity creates moat

- Local execution required (DISCOM relationships)

AI-Native from Day One

- Load forecasting, pricing optimization, compliance automation

- Agent-ready architecture for autonomous trading

- Data compounds into defensible moat

ESG Tailwind

- Every export MSME will need green energy proof

- First-mover in compliance infrastructure

- Regulatory relationship building

Integration with AIM Portfolio

- Cross-sell: MSMEs already on AIM for procurement → energy module

- Data enrichment: Energy patterns indicate business health

- Supplier intelligence: RE developer ratings and reliability

## Mental Models Applied

Zeroth Principles

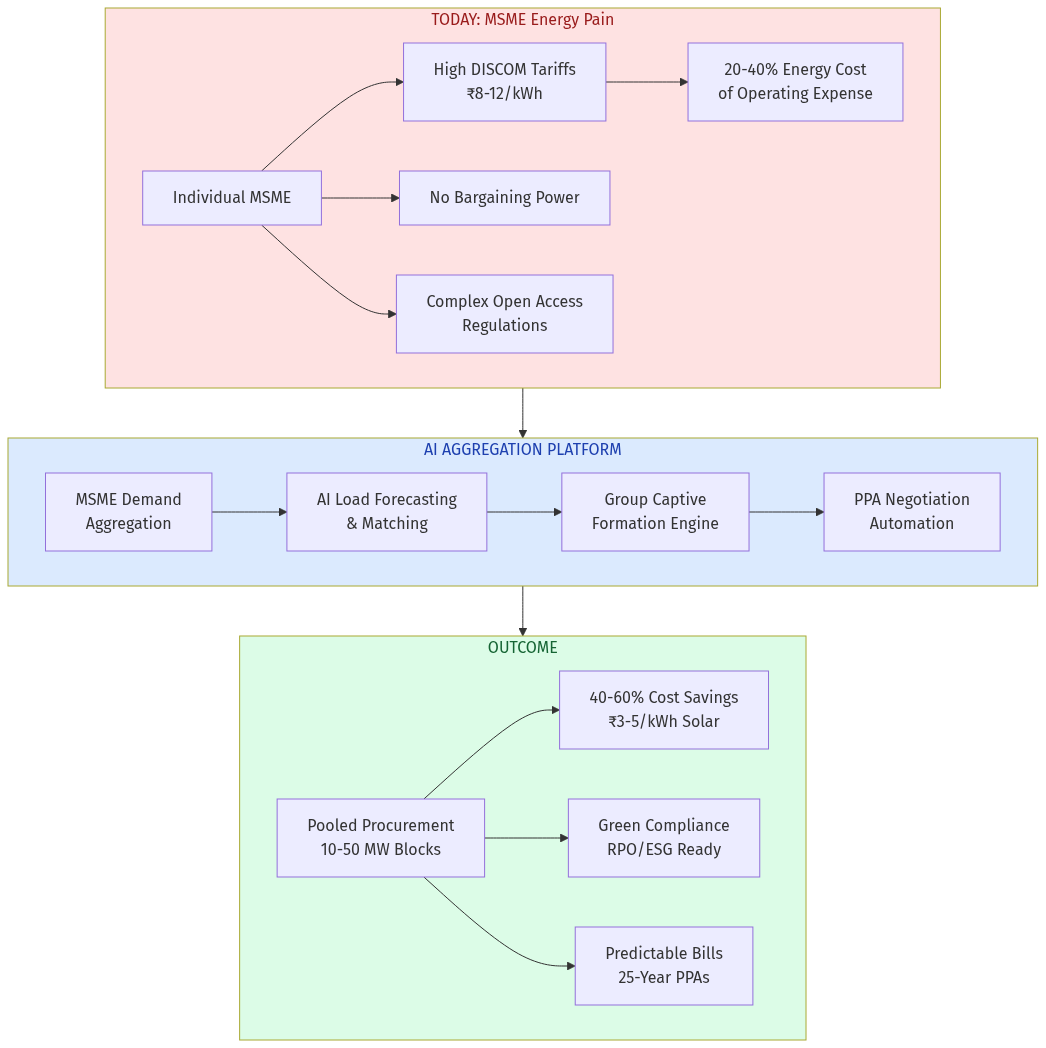

Question: Why don't MSMEs use solar already?

Assumption challenged: "Solar requires owning panels."

Zeroth insight: The barrier is procurement scale, not technology. Group captive removes the ownership burden—MSMEs just need a mechanism to pool demand.

Incentive Mapping

- DISCOMs: Lose high-paying industrial customers → will resist, delay approvals

- RE Developers: Want large, creditworthy offtakers → need demand aggregation intermediary

- MSMEs: Want savings but can't navigate complexity → need turnkey solution

- Government: Wants RPO compliance and green transition → policy tailwind

Distant Domain Import

Parallel: Group purchasing organizations (GPOs) in US healthcare. Hospitals pool demand for medical supplies, achieving 10-15% savings through collective bargaining.

Application: Same model for MSME energy—aggregate demand, standardize contracts, negotiate bulk pricing.

Falsification (Pre-Mortem)

Why might this fail?

DISCOM resistance blocks open access approvals

MSMEs churn from groups, destabilizing PPAs

RE developers prefer single large buyers

Regulatory changes eliminate cost arbitrage

Credit risk in group structure

Mitigations:

Start in progressive states (Gujarat, Rajasthan, Karnataka)

Long-term PPA commitments with exit penalties

Create guaranteed demand pools with escrow

Build regulatory affairs capability

Credit insurance and NBFC partnerships

Steelmanning (Why Incumbents Win)

Best argument against this opportunity:

"Fourth Partner and CleanMax will move downstream. They have developer relationships, execution capabilities, and capital. They'll build aggregation tools as a feature, not a product. A startup can't compete with vertically integrated players."

Counter: Large players optimize for ₹50 crore+ projects. MSME aggregation is operationally complex with thin initial margins. They'll ignore this segment until it's too late—classic disruption from below.

## Verdict

Opportunity Score: 8.5/10

Strengths

- Massive underserved market: 63M MSMEs locked out of cheap energy

- Regulatory tailwind: Open access rules, RPO mandates, CBAM

- Clear business model: Transaction fees + SaaS + embedded finance

- Defensible moat: Data + cluster relationships + regulatory expertise

- ESG urgency: Export MSMEs face 2026 deadline

Risks

- Execution complexity: Multi-stakeholder coordination

- Regulatory risk: State-level variations and DISCOM resistance

- Credit risk: MSME payment reliability in group structures

- Competition: Large C&I solar players could enter

Recommendation

Build this. Start with 3-5 industrial clusters in Gujarat and Tamil Nadu. Sign first 10 MW aggregated PPA within 6 months. The timing is perfect: solar costs at historic lows, ESG pressure rising, and no incumbent focused on MSME aggregation.

The winner will own India's MSME energy transition—a ₹2.5 lakh crore market undergoing structural disruption.

## Sources