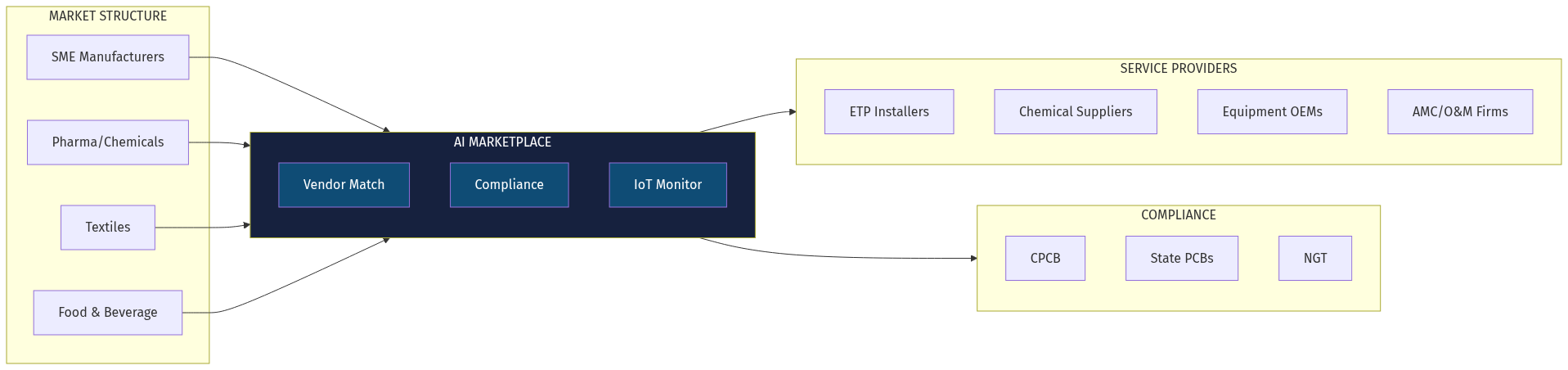

India's industrial water treatment sector is a paradox: critical infrastructure supporting $350B+ in manufacturing, yet operating through WhatsApp groups and phone calls. Zero Liquid Discharge (ZLD) mandates are tightening. Pollution Control Boards are getting aggressive. SMEs face closure threats for non-compliance.

The opportunity: Build the "Infra.Market for industrial water" — an AI-powered B2B marketplace connecting factories with ETP installers, chemical suppliers, and O&M providers, while automating the compliance nightmare that keeps plant managers awake at night.