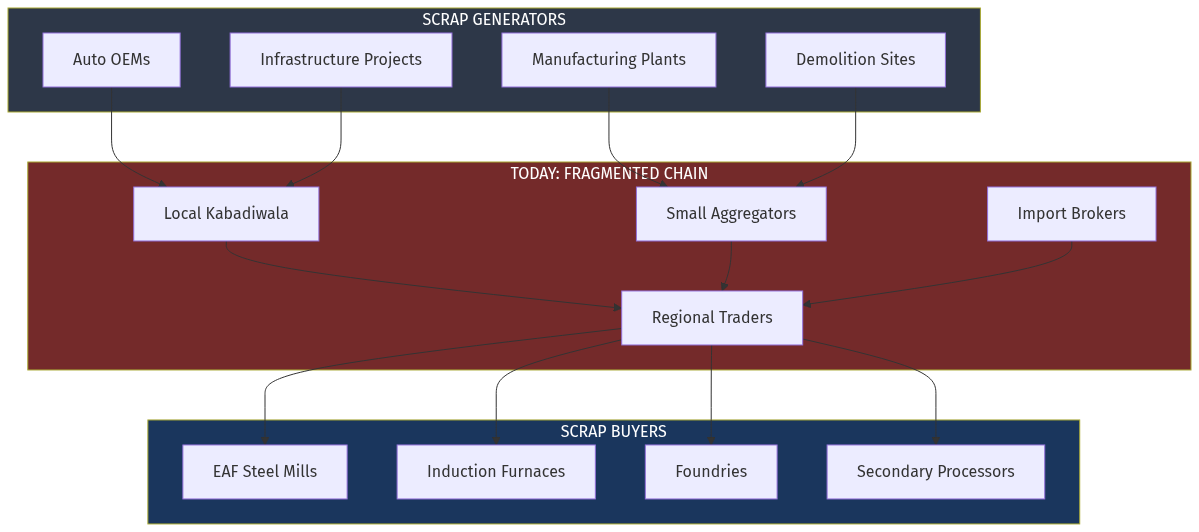

India's metal recycling market reached USD 14.14 billion in 2024 and will grow to USD 21.38 billion by 2030. Yet there's no dominant B2B marketplace connecting scrap suppliers to steel mills and recyclers. The existing system—a fragmented chain of kabadiwallas, aggregators, and dealers—suffers from price opacity, quality disputes, and cash-only transactions.

Meanwhile, steel mills are racing to adopt Electric Arc Furnaces (EAF) for green production, which requires 65 million tonnes of scrap annually by FY30. The supply gap means India must import 20-30 million tonnes yearly.

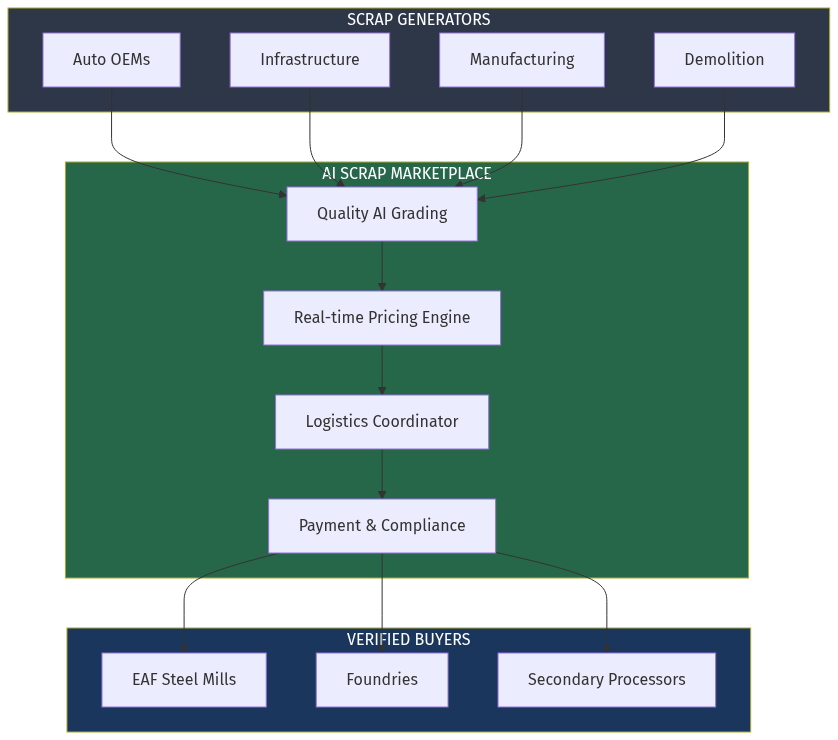

The opportunity: An AI-powered B2B marketplace that digitizes the scrap supply chain, provides real-time pricing indexed to LME, enables quality grading via image recognition, and integrates logistics. Think "IndiaMART meets Uber Freight" for scrap metal.