Zeroth Principles Analysis

Before examining current solutions, let's question the fundamental axioms:

Axiom 1: "Commercial vehicles are just another asset class for lending."

This is how lenders think. But a truck is not a house — it depreciates fast, moves across state borders, is driven by multiple people, and can be hidden or dismantled. Treating it like static collateral (like real estate) is fundamentally flawed.

Axiom 2: "The loan is the product."

Lenders focus on origination fees and interest rates. But the real value is in the asset lifecycle: refinancing, insurance, maintenance, resale, and replacement. Each transition is a new transaction opportunity.

Axiom 3: "Trust is established through paperwork."

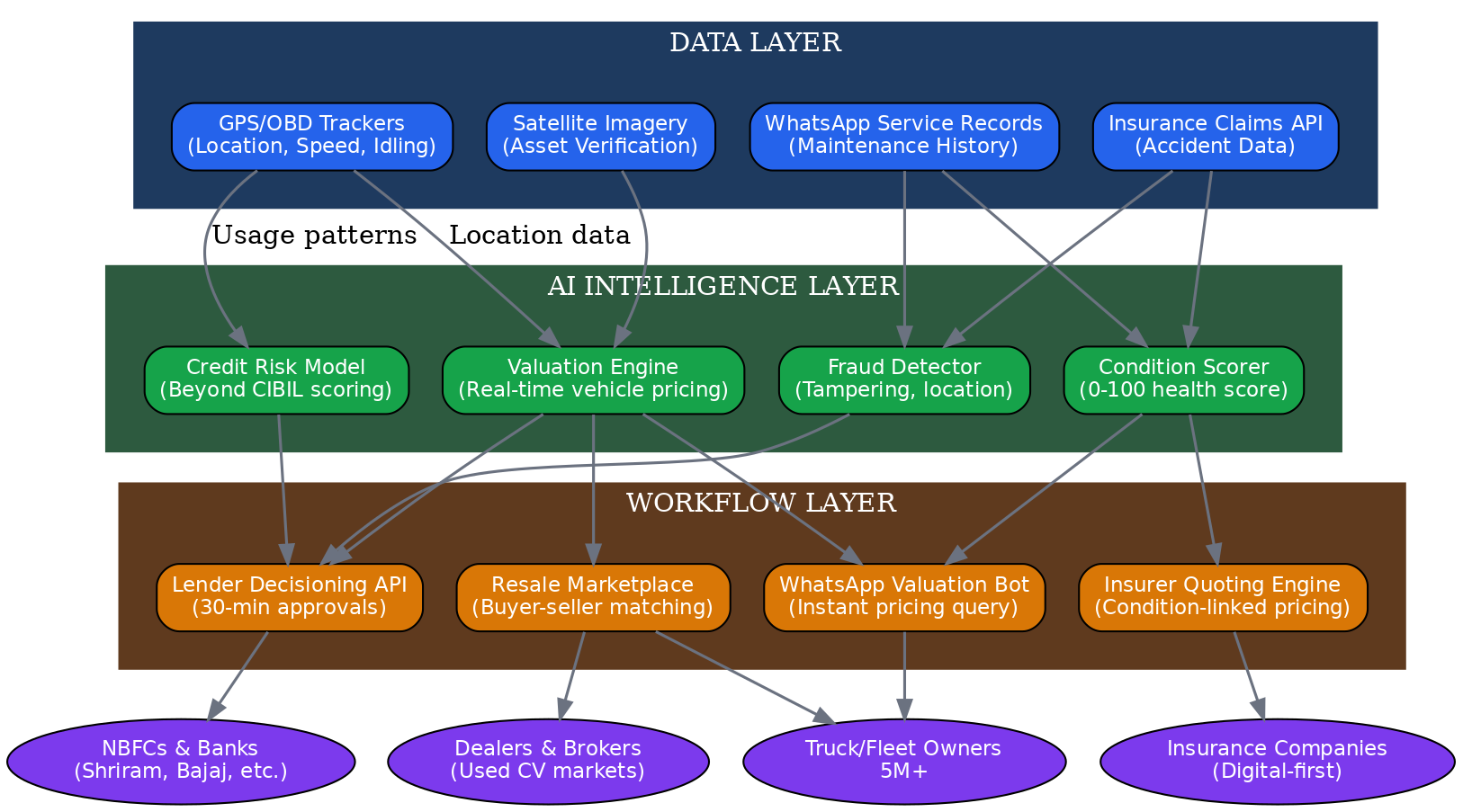

KYC documents, RC books, and chassis numbers. But these can be forged, outdated, or wrong. Real trust comes from verified, live data — location, usage patterns, maintenance history, resale comparables.

The Four-Part Breakdown

1. The Lender's Blindspot

- No real-time asset tracking (lenders don't know where the vehicle is)

- Manual inspection cycles every 6-12 months (expensive, unreliable)

- No usage data (highway kms vs. city kms, load patterns, idling time)

- Resale value guessing based on outdated data

- Recovery in default: vehicle may be in a different state, dismantled, or "lost"

2. The Owner' Dilemma

- Can't prove vehicle condition to get better refinancing rates

- Stuck with original lender at high interest rates (no competitive refinancing market)

- Manual maintenance tracking (service records scattered across receipts)

- No market visibility on resale value

- WhatsApp-based "my truck value kya hai?" queries with no reliable answer

3. The Insurer's Risk

- Pricing policies with minimal vehicle-specific data

- Claims settlement disputes over "pre-existing damage" vs. new damage

- No way to verify accident history or odometer tampering

- Fraud: "total loss" claims on vehicles that are still running

4. The Dealer's Fragmentation

- Thousands of small dealers operating through WhatsApp groups

- No standardized pricing data across regions

- Buyer-seller matching is slow and trust-dependent

- Financing for resale transactions is ad-hoc