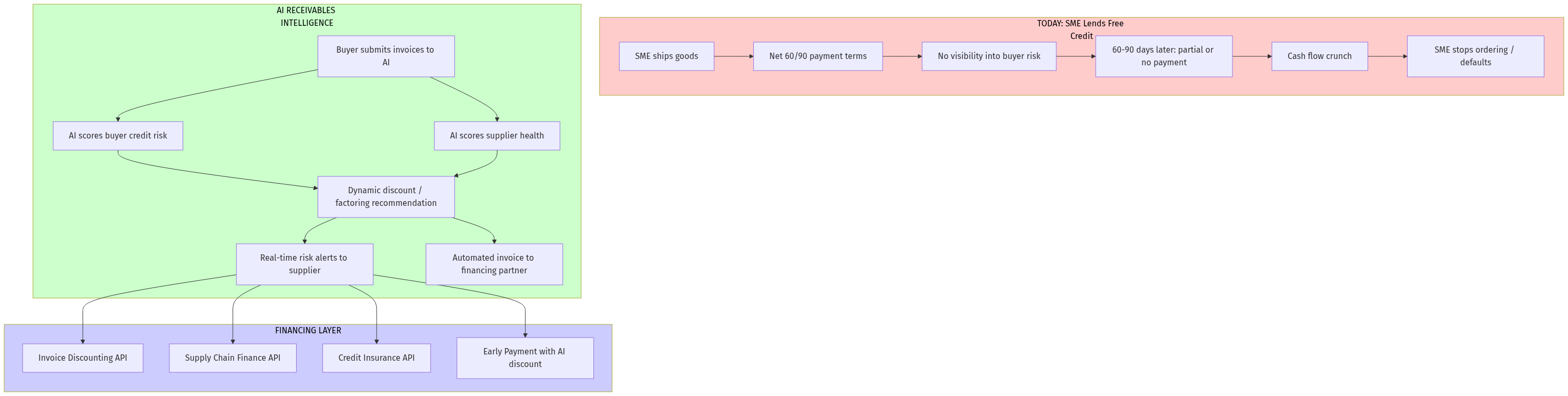

Indian SMEs face a structural paradox: they generate revenue but starve for cash. The root cause is the Receivables Gap — suppliers ship goods worth crores, then wait 60-90 days for payment while their buyers (often large corporates or government entities) sit on cash. Meanwhile, the supplier's staff can't eat, can't buy raw materials, and can't scale.

Current "solutions" are broken:

- Bank loans: Require collateral, take 4-8 weeks, rejection rates > 60% for SMEs

- Invoice discounting: Requires physical documentation, expensive (18-36% p.a.), available only to large companies

- Supply chain finance: Only for tier-1 suppliers of large corporates

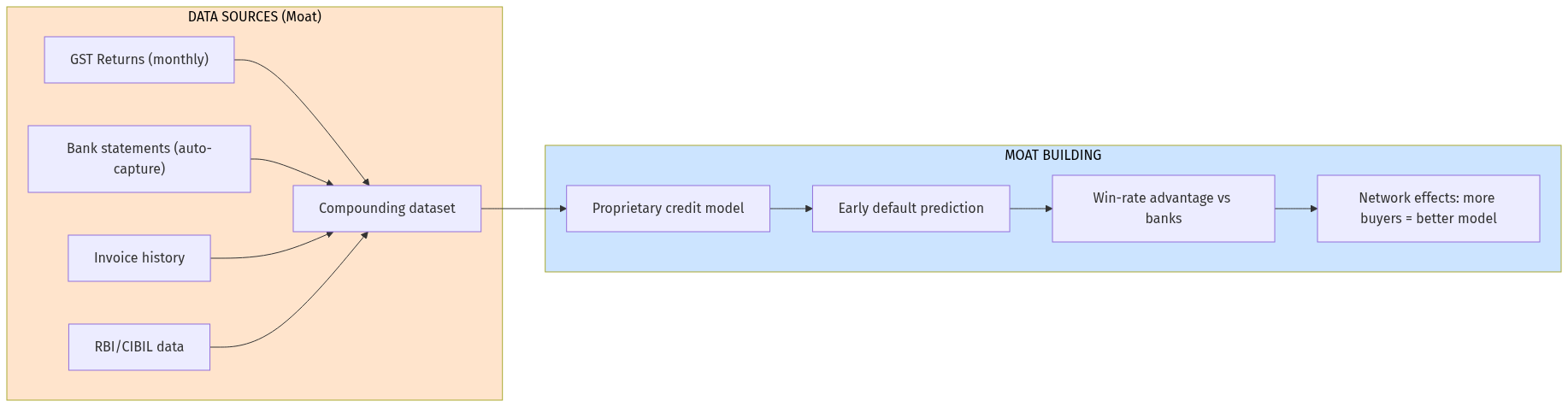

An AI-powered receivables intelligence platform targeting this gap has the potential to become the Bloomberg for Indian B2B credit — except it's free for suppliers and earns from financing partners.

Opportunity Score: 9/10