AIM.in is building India's largest structured B2B discovery platform. FreightGuard fits the ecosystem in several ways:

1. Vertical integration: Logistics is a core B2B workflow. Every manufacturer, distributor, and retailer moves goods. Adding freight audit to the AIM portfolio creates a sticky, recurring workflow that drives daily engagement.

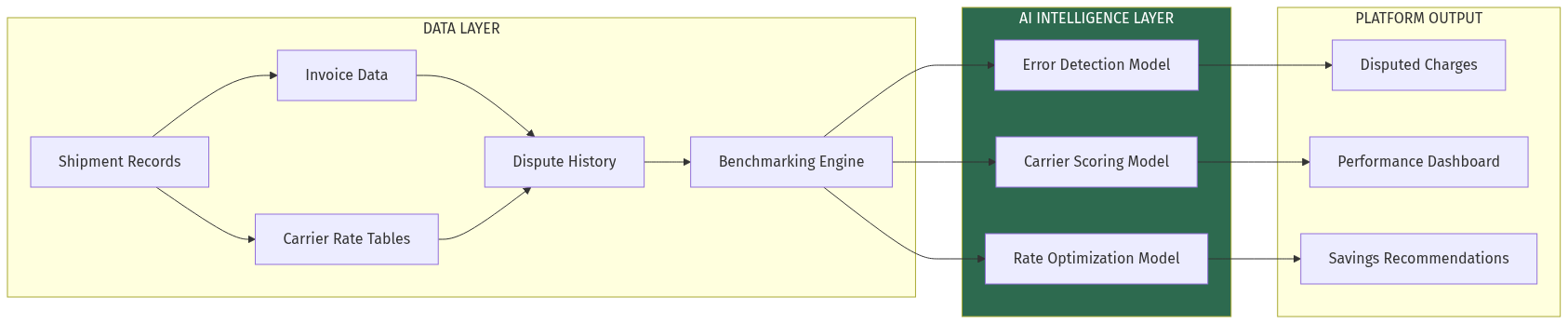

2. Data synergy: AIM already has domain intelligence on Indian companies. FreightGuard's carrier billing data complements this — giving insight into which companies ship what volumes, which carriers they use, and how their logistics costs compare.

3. WhatsApp-native distribution: AIM's WhatsApp-first approach maps perfectly to FreightGuard's onboarding model. A logistics manager who discovers AIM for one workflow can add FreightGuard without leaving WhatsApp.

4. Network effects across verticals: A manufacturer using FreightGuard shares benchmarking data with their 3PL. The 3PL manages freight for 10 other companies. FreightGuard is now embedded in 11 companies without additional acquisition cost.

5. Natural upsell path: FreightGuard users who need carrier comparison eventually need carrier sourcing. AIM's domain discovery pipeline routes them to vetted carriers on-platform.

## Falsification (Pre-Mortem)

Scenario: Assume 5 well-funded competitors entered this space and failed. Why?

Enterprise-only pivot: Competitors targeting large enterprises hit long sales cycles (6-12 months) and high implementation costs. The mid-market is more nimble but needs self-serve onboarding.

Integration-first strategy: Building integrations before achieving product-market fit caused cash burn to exceed user growth. WhatsApp-first > integration-first.

Carrier-side data lock-in: Competitors tried to build carrier partnerships first, getting locked into one carrier's ecosystem. Shipper-first > carrier-first.

Pricing misalignment: Competitors charged high success fees (30-40%) that made shippers feel like they were paying twice. Keep success fees at 10-15%.

Ignoring dispute friction: Building the audit but not the dispute resolution workflow left users with insights but no recovery. End-to-end > insight-only.

Steel Manning (Why Incumbents Might Win):

Large TMS players (Cassiopae, Blue Yonder) could add freight audit modules to their existing platforms and win on relationships. However, their enterprise-first pricing (Rs 50L+ per year) and implementation timelines (6+ months) keep the mid-market accessible. The TMS incumbents have no mid-market strategy — their entire GTM is built for large enterprises.

## Verdict

Opportunity Score: 7.5/10

Rationale:

- Market size: $3.2B mid-market annual spend with 4-7% error rate. Large enough to build a Rs 100+ crores ARR business.

- Timing: AI cost collapse + GST formalization + D2C growth + API infrastructure maturity. These tailwinds are concurrent for the first time.

- Competition: Wide open white space. No Indian mid-market-focused freight audit platform exists.

- Moat: Data network effects from carrier benchmarking create 2-3 year defensibility.

- Risk: Carrier API reliability (Indian carriers have inconsistent APIs). Mitigation: build hybrid extraction (API + document parsing).

- Execution risk: User acquisition in the mid-market requires strong product-led growth and WhatsApp distribution. Execution hinges on achieving viral coefficient > 1.2.

Recommendation: Build. Start with WhatsApp-first MVP, validate with 10-15 beta users, measure recovery rate. If 70%+ recovery rate achieved with

## Sources