Zeroth Principles

Q: What if we assumed that debt recovery = information problem, not legal problem?

A: Most small defaults are "forgotten" not "deliberate." Smart nudges recover more than legal threats. An AI system that gently reminds, offers a path, and tracks commitments outperforms one that threatens.

Incentive Mapping

Q: Who profits from the status quo?

A: Legacy BPO collections agencies profit from high agent headcount. Lenders profit from appearing "tough" on defaults. Banks profit from writing off loans and raising capital instead of recovering efficiently.

Our incentive: Recover more money at lower cost, which is directly aligned with lender AND borrower interests.

Distant Domain Import

The AI pattern here mirrors:

- Spam filtering (Gmail): Classifying messages by probability of action. Collections is the same — probability an account resolves.

- E-commerce abandoned cart recovery: Dunning sequences with AI-generated personalized reminders are proven to work at scale.

- Medical adherence: Persuading patients to take medicine is like persuading borrowers to pay — both need trust restoration.

Falsification (Pre-Mortem)

Assume 5 well-funded startups failed here. Why?

Regulatory crackdown on digital lending (DCA 2024 provisions) made WhatsApp outreach risky

Lenders refused to share default data (privacy/sensitivity)

Borrower churn was too high — too much trust damage before platform could intervene

AI couldn't handle方言 (regional language) complexity

Settlement negotiation required too much human judgment

Mitigation: Build RBI-compliant audit trails, anonymized model training, multilingual with Hindi-first, settlement as human-in-the-loop.

Steelmanning

Why might incumbents win?

Existing relationships between banks and legacy BPOs are deep and resistant to change

Collections is politically sensitive — lenders fear borrower backlash from "robots calling me"

RBI compliance requirements create barriers for new entrants

Small NBFCs lack digital maturity to adopt SaaS

Counter: Start with digital-native NBFCs, demonstrate recovery rate improvement with hard data, expand from proof points.

Anomaly Hunting

What's strange about this market?

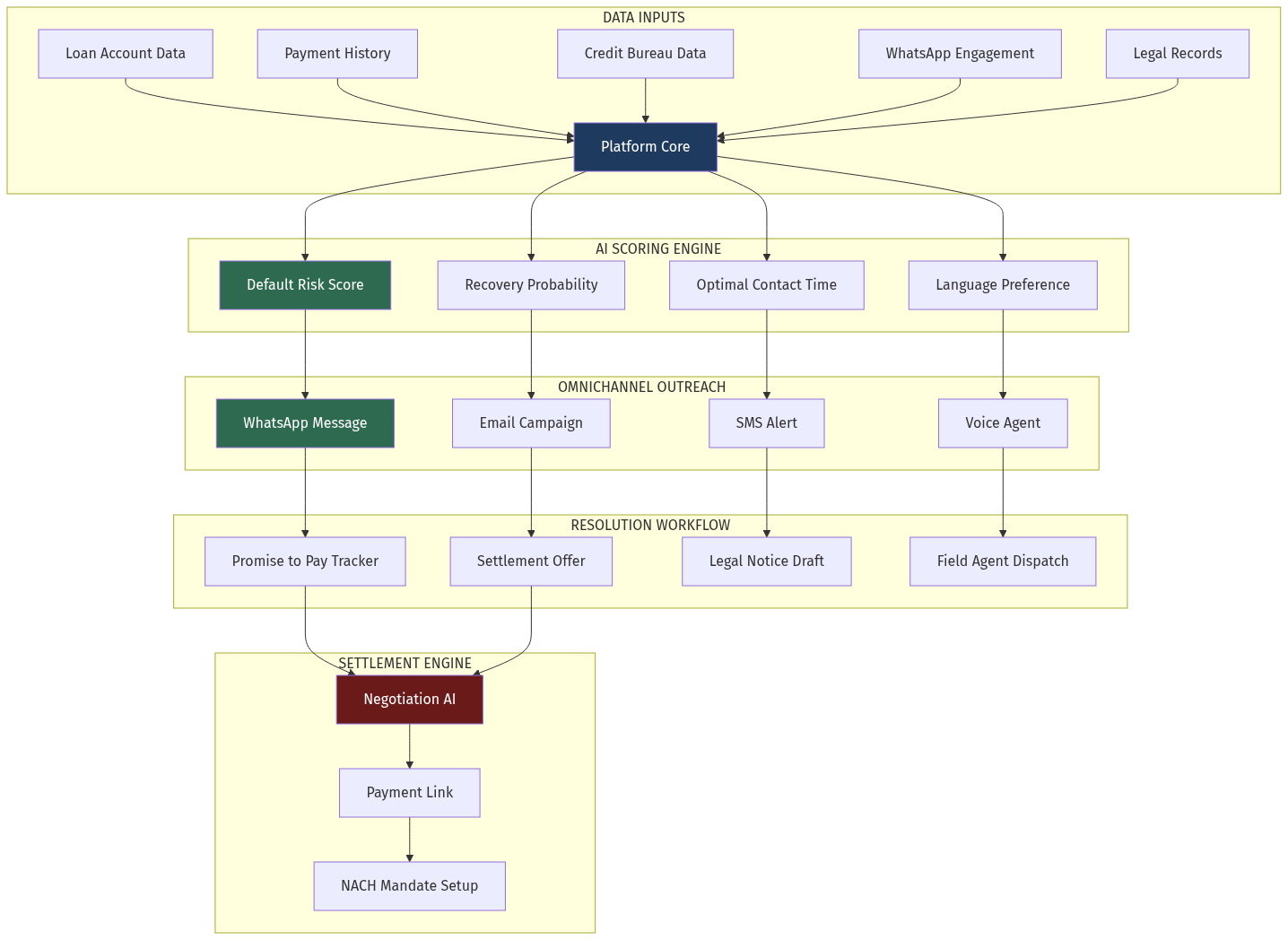

India has 530M+ WhatsApp users — the world's largest messaging platform — but NO AI-native collections layer exists on it. Every lender manually sends WhatsApp messages with no automation, no tracking, no intelligence. That's the anomaly: the most powerful channel is completely untapped.

## Verdict

Opportunity Score: 8/10

This is a high-urgency, high-conviction opportunity. The conditions are uniquely aligned:

NPA cycle at peak = desperate demand for better tools

WhatsApp penetration makes India uniquely addressable

No AI-native collections platform exists in India

Clear ROI (recover X% more, save Y% on agents)

Recurring revenue model with success fees

High data moat over time

Risks: RBI regulatory uncertainty, borrower trust deficit, lender adoption friction.

Best Entry Point: Partner with 2-3 mid-sized NBFCs for pilots, demonstrate recovery improvement with hard data, expand via network effects.

Avoidable Trap: Don't build legal tech first. Legal escalation is the LAST step, not the first. Start with intelligent soft collections — WhatsApp, voice AI, and PTP tracking — where most recoveries happen.

Time to First Revenue: 4-6 weeks with 2 paying pilots.

## Sources