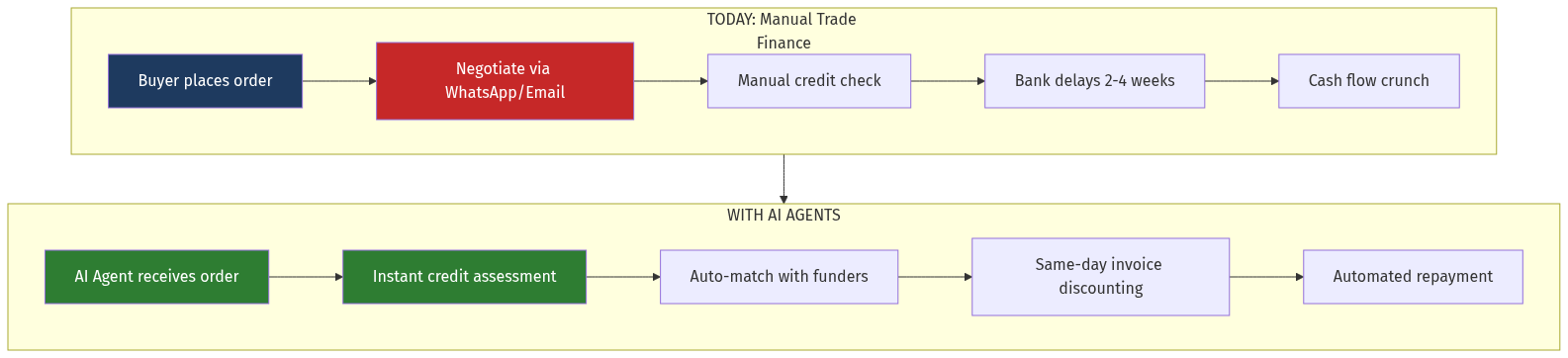

India's 63 million SMBs face a silent crisis: Rs 3.2 lakh crore ($380 billion) in unpaid invoices are stuck in manual collection cycles. Large buyers延时 60-90 days while suppliers starve for working capital. Traditional banks reject 70%+ of SMB credit applications due to opaque risk assessment.

The opportunity: An AI-powered trade finance platform that:

- Instantly assesses invoice authenticity via AI document analysis

- Matches unpaid invoices with a network of alternative funders

- Provides same-day discounting (vs. 2-4 week bank delays)

- Uses WhatsApp-native workflow for 85% of Indian SMBs