The Indian SMB credit market is a $100B+ opportunity stuck in manual paperwork. 75 million SMBs need working capital, but:

- Banks reject 80%+ of SMB loan applications

- NBFCs charge 24-36% interest (predatory pricing)

- Loan disbursement takes 15-45 days in manual processes

- No AI-native platform exists for SMB credit in India

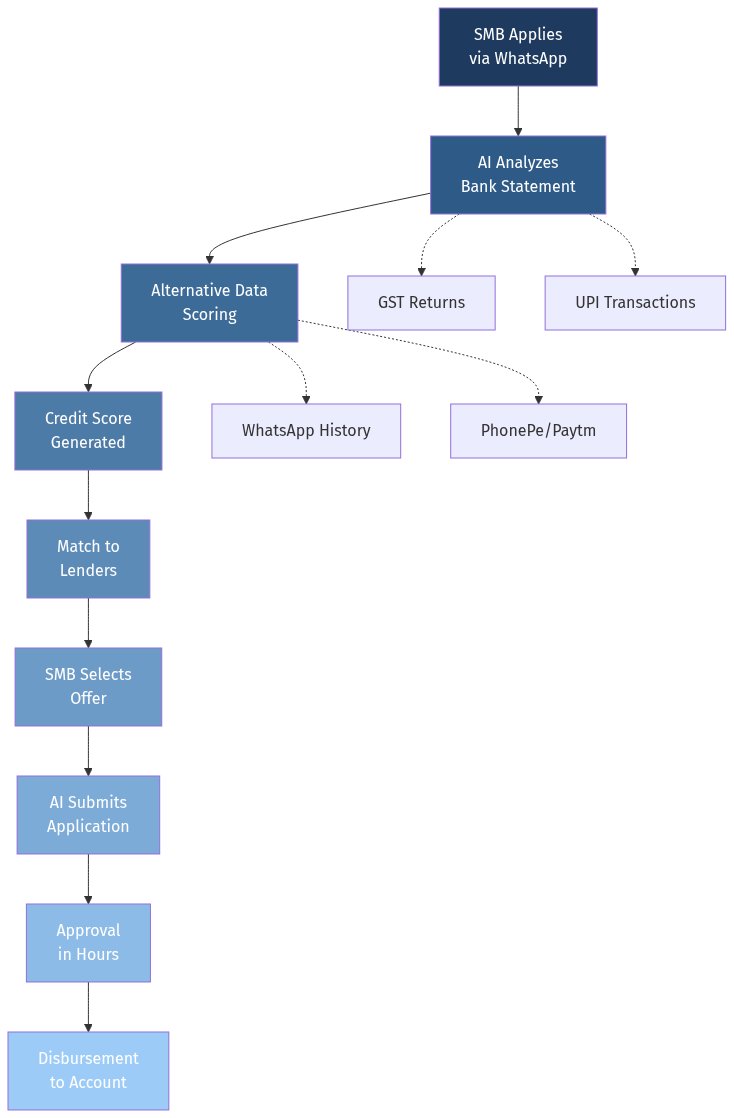

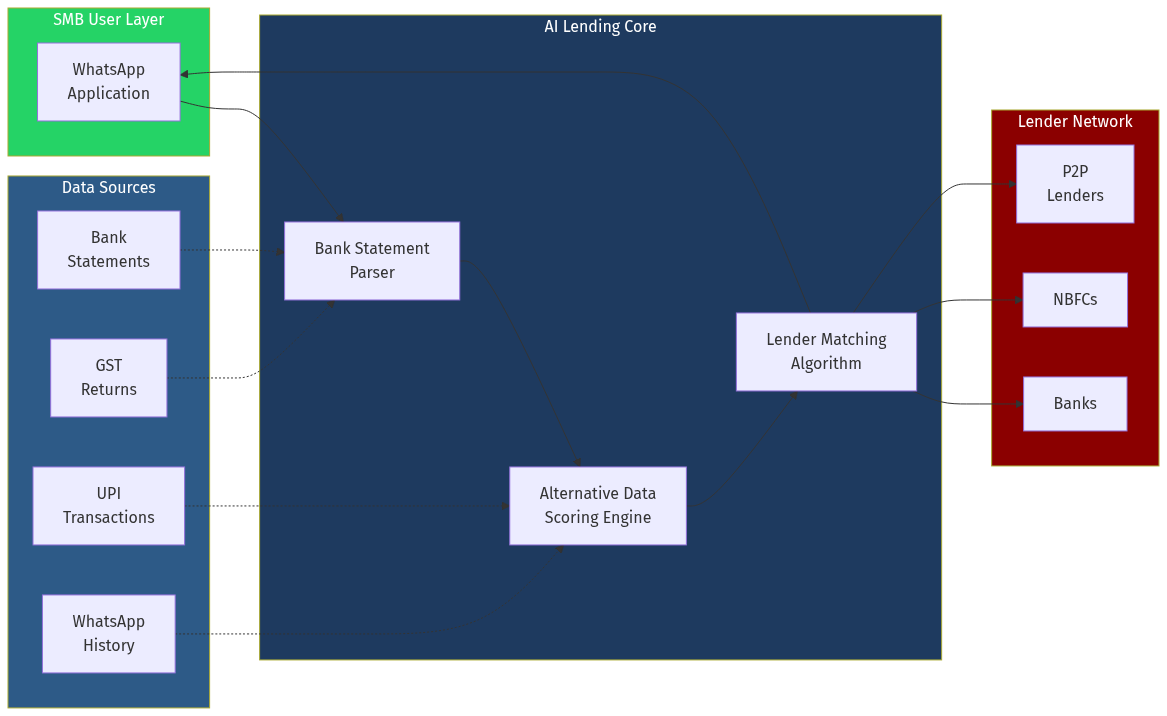

- Auto-analyze bank statements, GST returns, and invoices

- Underwrite SMBs in real-time using alternative data

- Match borrowers with the right lenders (banks, NBFCs, P2P)

- Close loans in hours, not weeks